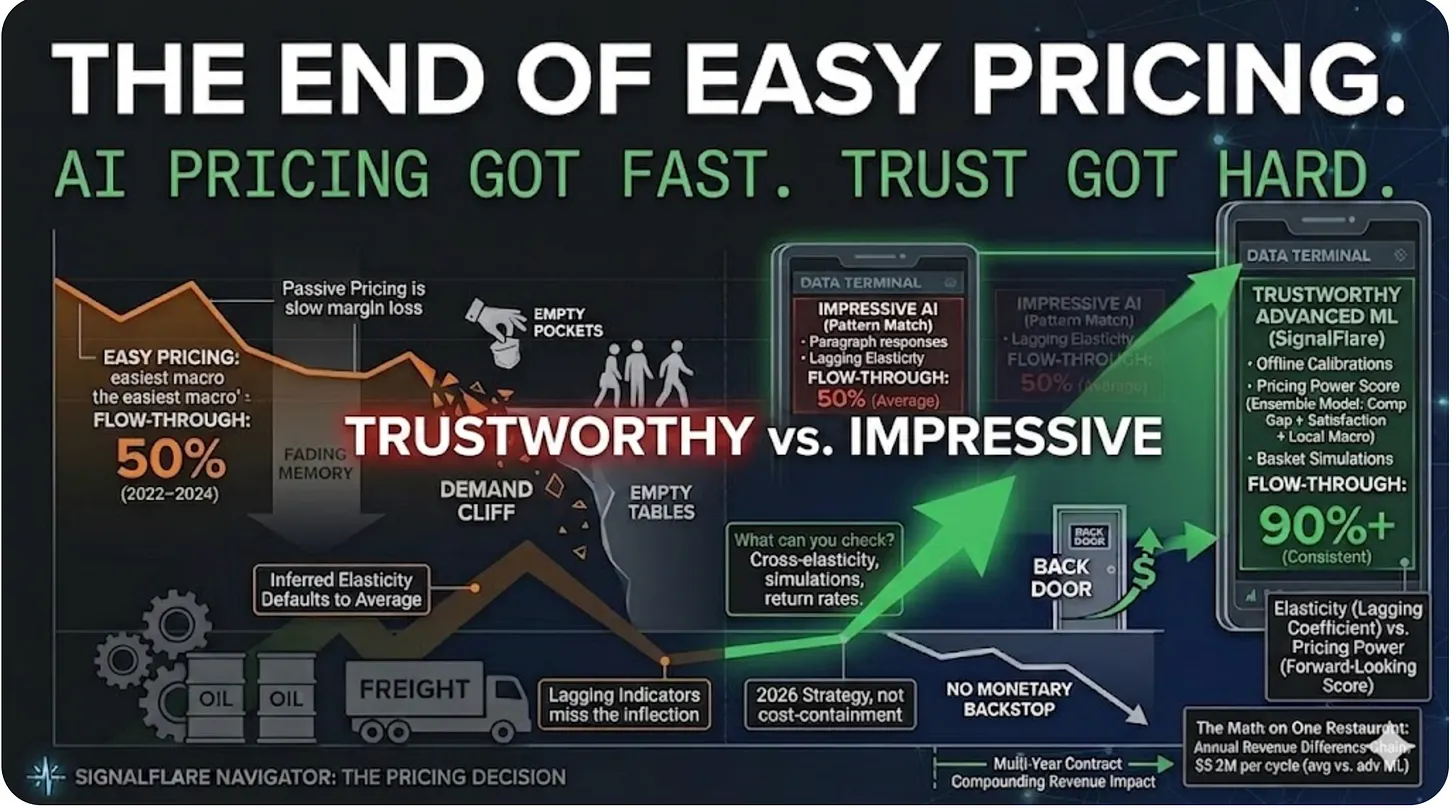

Restaurant Inflation Still Running Hot

Food away from home inflation hit 3.9% year-over-year in July. That's down from recent peaks, but still nearly double the Federal Reserve's 2% target for overall CPI. Full-service restaurants are seeing 4.4% price growth compared to 3.3% at limited-service operations.

That gap matters. It signals casual dining operators face higher cost pressures with less pricing flexibility than fast-food chains.

For operators, "slowing inflation" misses the point. Prices are still rising. Just at a slightly slower pace.

CPI Soft, PPI Surges — The Tell-Tale Split

Consumer prices rose a manageable 0.2% month-over-month in July. Producer prices told a different story, spiking 0.9% — the largest monthly increase since June 2022.

This gap reveals the current reality: businesses are absorbing tariff costs instead of passing them through to customers - but that absorption pattern is temporary. Margins only compress so far.

Why the Consumer Impact Hasn't Hit Yet

Two factors explain the delay:

1. Implementation Lag — The April tariff announcements created a gap between policy and price reality.

2. Inventory Front-Loading — Importers stockpiled goods before tariffs took effect. This showed up as artificial GDP growth in Q2 when imports later plunged over 30%.

This wasn't organic economic strength. It was an accounting effect that I predicted back in April would create exactly this mirage.

Producer Data Shows What's Coming

The July PPI breakdown reveals the inflationary pipeline:

Services: +1.1% month-over-month (largest gain since March 2022)

Trade services margins: +2.0% (direct tariff pass-through effect)

Machinery and equipment wholesaling: +3.8%

These aren't random price spikes. They're systematic adjustments as wholesalers and retailers prepare for higher import costs.

Labor Market Adds Complexity

Employment revisions paint a weaker picture than headlines suggested. May and June payrolls were revised down by 258,000 jobs — the largest two-month adjustment since 1968. Three-month average job growth now stands at just 35,000 monthly, down from 111,000 in Q1.

Continuing jobless claims hit 1.974 million in July, the highest level since November 2021.

Weaker employment could slow consumer demand. That might be the only thing keeping price pressures in check — but it's a blunt instrument.

The Fed's Impossible Position

Markets have priced in an 88% probability of rate cuts in September despite building producer inflation. JPMorgan estimates consumer pass-through will reach 67% by October, up from just 22% in June.

If that timeline holds, the consumer price impact arrives just as the Fed loosens policy. Major institutions now project core inflation reaching 3.2-3.9% by year-end, with 0.7 to 1.5 percentage points directly attributable to tariffs.

That's a challenging setup for policymakers.

Bottom Line

The data tells the Story of a tough road ahead:

Restaurant inflation remains elevated at nearly double Fed targets

Producer prices are surging while consumer prices stay contained

The Q2 GDP boost from inventory buildup was artificial

Tariff costs are accumulating at wholesale levels

Employment is weaker than initially reported

The consumer price impact is coming. The only questions are when and how severe. JPMorgan's October timeline for meaningful pass-through gives us a window.

For restaurant operators, the message is straightforward: the current pricing environment won't last. Plan accordingly.

The mirage is fading. Reality shows up on the check.

Read the original post and subscribe for updates here.

Share