Restaurant spending is discretionary. It is also one of the more reliable early signals of how consumers are actually behaving — not how they report feeling in a survey, but what they do when household budgets tighten and something has to give. When gas prices spike or real wages fall, restaurants tend to feel it first and feel it visibly, in visit frequency, in check size, and in which segments gain traffic while others lose it. That makes the patterns worth watching even if you have no particular stake in the restaurant industry itself.

What follows is built on that premise. The analysis draws on real purchase data, consumer behavior signals, and probability-weighted scenario modeling to look at what a significant energy shock is doing to consumer decisions right now. Perhaps more importantly, what is the potential lag-effect of this magnitude of impact as the the March CPI gasoline index posted its largest one-month increase since BLS records began in 1967? The restaurant industry is the lens into consumer behavior: when a consumer with no savings buffer absorbs another two to four dollars per fill-up, where does the spending go, and what does that tell us about where the economy is actually headed?

The Ground Condition Before March

The restaurant industry entered 2026 with a probability-weighted traffic forecast already pointing to negative 3.2 percent for the year. That figure was not a reaction to any single event. It was the output of three structural conditions that had been building for two years.

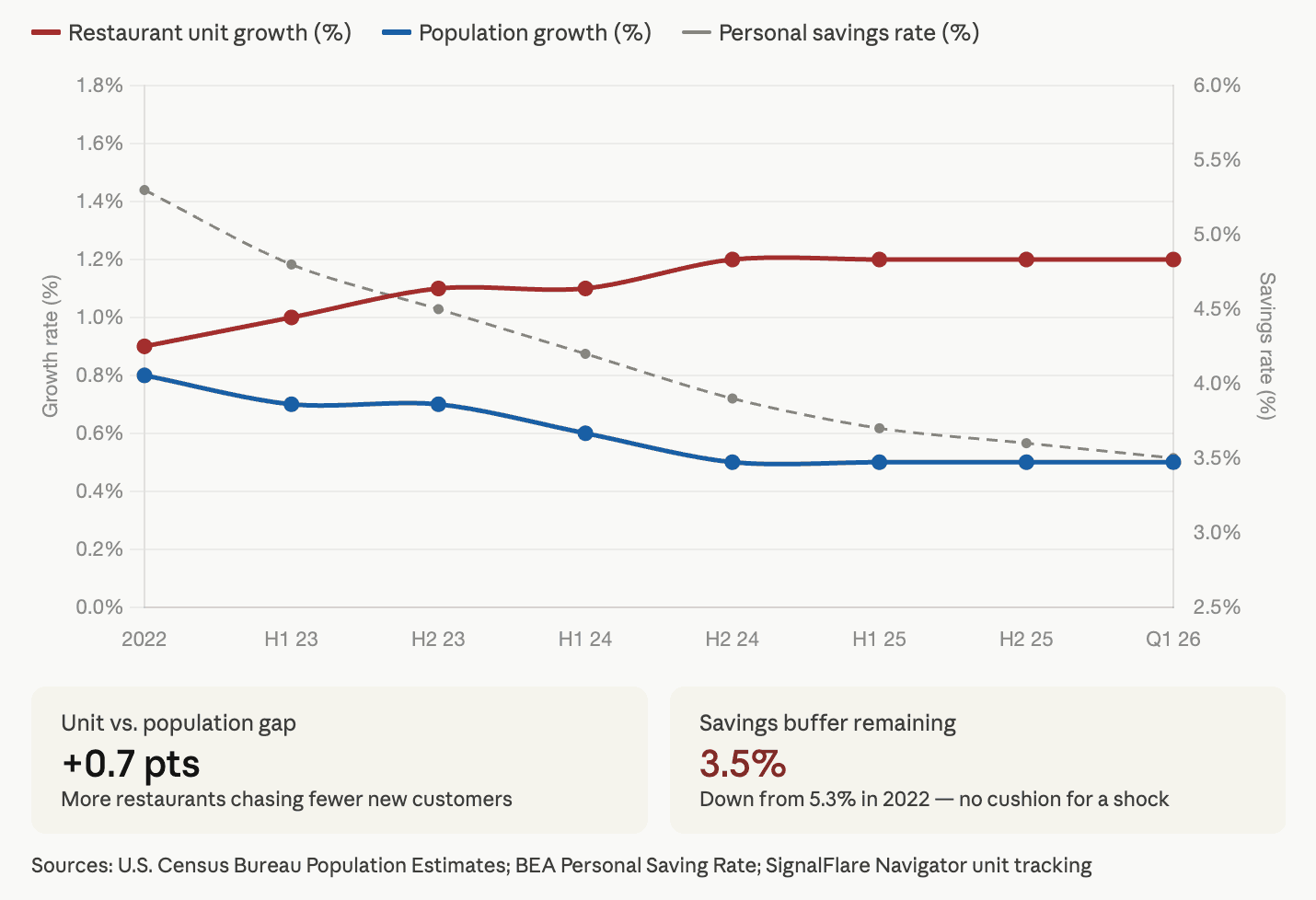

Restaurant unit count had been expanding at roughly 1.2 percent annually while national population growth decelerated to 0.5 percent in 2024–2025, a 35 percent drop from the prior year’s pace, according to U.S. Census Bureau estimates. Even the fastest-growing Sun Belt markets were slowing. Florida’s population growth rate dropped 43 percent year-over-year. Texas dropped 36 percent. The organic customer inflow that operators built expansion models around was arriving at lower rates than projected. In most trade areas, market share had become the only viable growth mechanism.

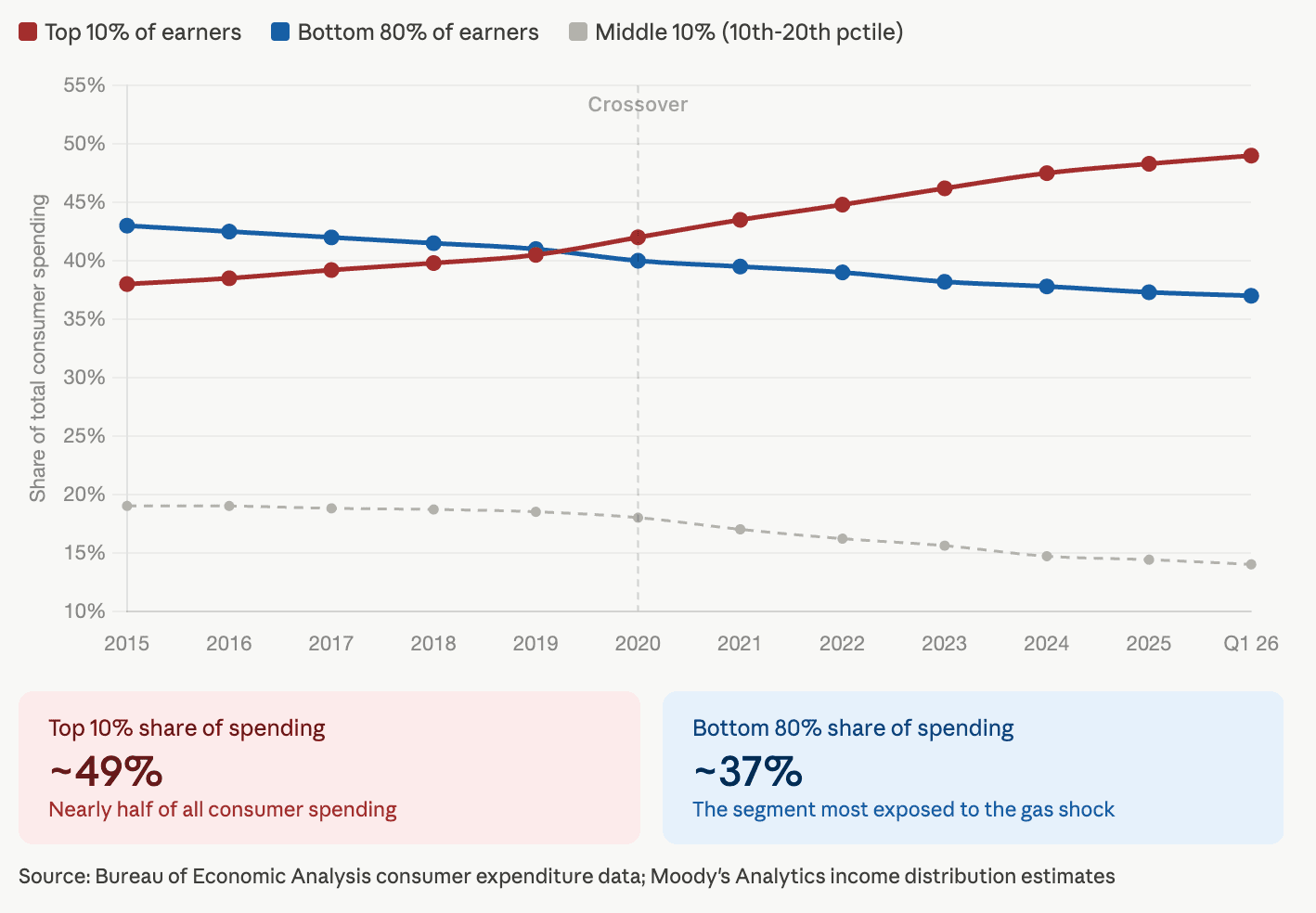

The consumer side carried a parallel problem. The bottom 80 percent of U.S. earners account for roughly 37 percent of consumer spending. The top 10 percent account for nearly half, according to Bureau of Economic Analysis data. Those lines crossed around 2020 and have been diverging since. The lower-income consumer — the core quick-service customer — had already been managed through discounting and value offers before 2026 began. The personal saving rate sat at 3.5 percent and falling. The discount was doing the work that income growth was not. There was no buffer.

Fast casual was getting squeezed from both directions — too expensive for value-seeking lower-income consumers, not differentiated enough to hold higher-income diners. Casual dining had been winning on aggressive bundling that undercut fast casual price points while delivering table service. The traffic share data made the trend visible: through February 2026, the burger category had climbed to 31 percent of restaurant traffic, up from 27.1 percent in January 2025, based on SignalFlare Navigator transaction records. Coffee had dropped from 13.9 percent to 12.7 percent. Sandwiches were losing share. The trade-down into value QSR was already underway and accelerating before any external shock registered.

That was the ground condition. Then something hit it.

What the March CPI Data Actually Tells Us

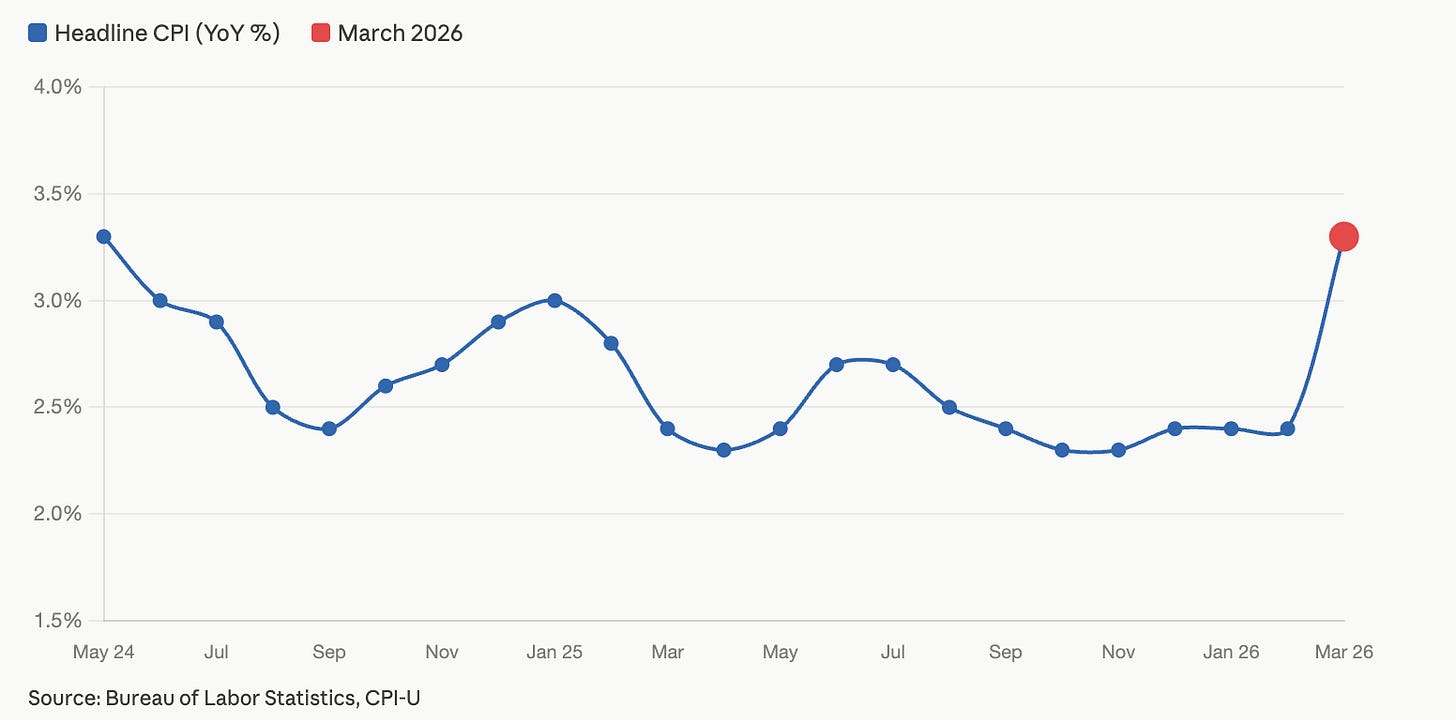

The March Consumer Price Index, released by the Bureau of Labor Statistics on April 10, 2026, landed with a headline number that stopped two years of gradual progress cold. Headline CPI rose to 3.3 percent year-over-year, up from 2.4 percent in February — the highest reading since May 2024. The gasoline index rose 21.2 percent in a single month, the largest one-month increase in BLS records dating to 1967.

The cause - Middle East military actions beginning February 28th sent Brent crude from $73 per barrel to nearly $97 over roughly six weeks, according to Energy Information Administration daily spot price data. The national average for regular gasoline moved from $2.98 to $4.15 over the same period. Resolution remains uncertain.

What March CPI captures is the pump price. What April through Q3 will capture is everything downstream. Supply chains, food input costs, and transportation logistics absorb energy price increases with a two-to-six month lag. Trucking costs, packaging, food distribution, and restaurant margin compression follow in sequence. The March number is not the full impact. It is the announcement of what’s to come.

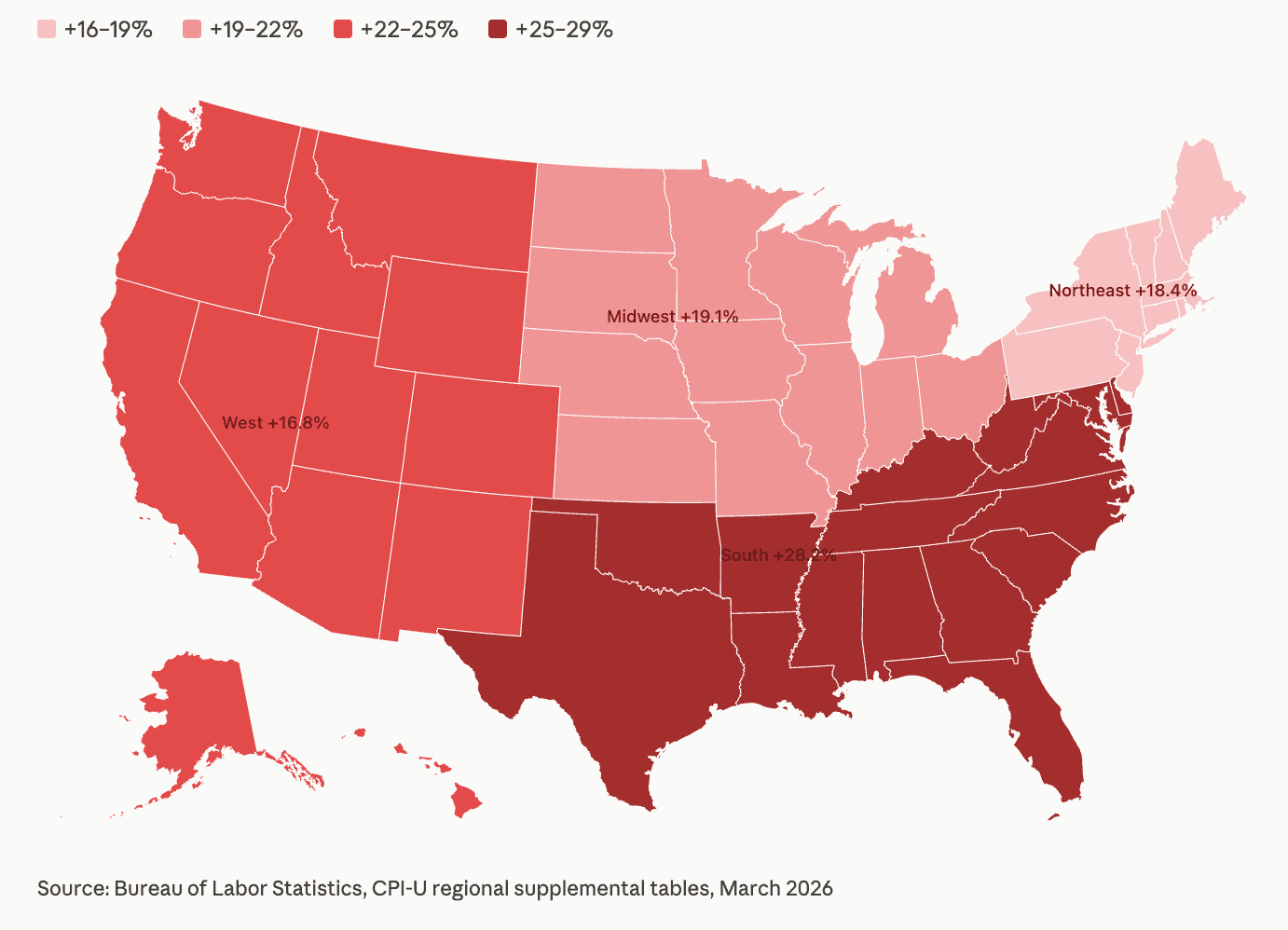

The regional picture matters more than the national figure. The South recorded the largest gasoline index increase of any U.S. Census region — up 28.2 percent for the month, with overall energy up 14.2 percent, according to BLS regional CPI supplemental tables. The South had been the restaurant industry’s most reliable traffic region for two consecutive years, consistently leading same-store sales growth. It is also the most drive-dependent, least transit-served region in the country, with the highest concentration of lower-income consumer segments already under the most financial pressure. The shock did not land evenly. It landed hardest where the industry had been leaning most.

Real average hourly earnings fell 0.6 percent in March, according to BLS. For households running a 3.5 percent savings rate, a gas increase of this scale does not get absorbed by income growth. It comes out of something else. The University of Michigan Consumer Sentiment Index fell to 47.6 in early April — the lowest reading in the survey’s history — with one-year inflation expectations jumping a full percentage point in a single month to 4.8 percent. When consumers revise their inflation expectations upward that sharply, their spending behavior tends to adjust ahead of the actual price changes, not after.

Where the Shock Is Landing

The gas shock did not arrive into a healthy industry. It arrived into one already running a structural deficit across units, consumers, and competitive positioning.

The lower-income, drive-dependent, suburban consumer — the same customer the industry was already working hardest to retain — is now absorbing another two to four dollars per fill-up from a budget that had no room for the subtraction. The impact concentrates most heavily in the South, which had been carrying the industry’s traffic numbers while other regions softened.

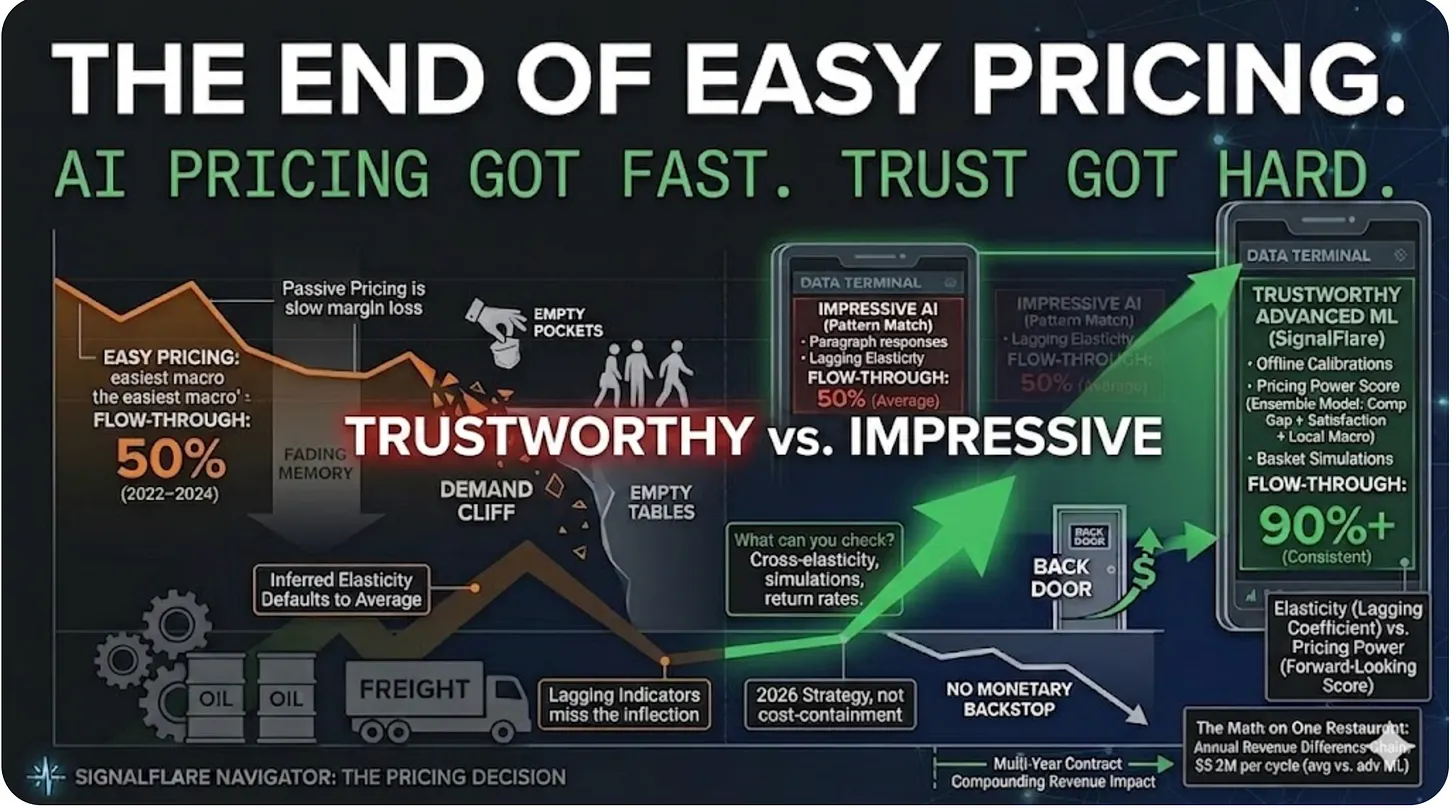

SignalFlare Navigator transaction data shows a consumer who had already started making different decisions before the gas shock registered. Fewer visits to coffee and sandwich. More visits to burger. More deliberate about when and where to spend. The gas shock does not reverse that pattern. It accelerates it — and narrows the margin for error for any brand not sitting clearly on the value end of the spectrum or the experience end. Brands in the middle are the most exposed.

Translating the Energy Shock Into a Traffic Estimate

Converting an energy shock into a traffic forecast is not precise work. The estimate below draws from a composite of academic research on gasoline price elasticity and SignalFlare Navigator transaction and consumer behavior data — weighted by historical predictive accuracy against observed outcomes. The composite puts the traffic impact of a 10 percent gasoline increase at roughly 0.9 percent, with a lag of six to eight weeks.

Applied to the March gasoline figures, the directional picture is clear. At the national level, a 21.2 percent gasoline increase implies roughly a 1.9 percent incremental traffic headwind. In the South, where the gasoline index rose 28.2 percent, the implied headwind is closer to 2.5 percent — and the South is the region the industry has been leaning on most.

Two forces partially offset the gross headwind. Trade-down pushes consumers down the price ladder, not always out of restaurants entirely. The burger category had already captured that movement, reaching 31 percent of industry traffic through February before the shock registered. Closure redistribution provides a second offset: when a unit closes, roughly 40 percent of its traffic moves to surviving competitors in the trade area rather than leaving the market. Both effects are real. Neither eliminates the directional pressure.

Exposure is not uniform across segments. Coffee, sandwich, and pizza categories carry the most risk — discretionary visit occasions, already losing traffic share, high drive-dependence in the customer base. Value burger QSR is most insulated, particularly in urban and transit-accessible markets where gas sensitivity is lowest and the trade-down tailwind is strongest. Fast casual sits in the most complicated position: caught between value QSR below and casual dining above, with less price distance from either than it held two years ago.

Where the Model Stands Now

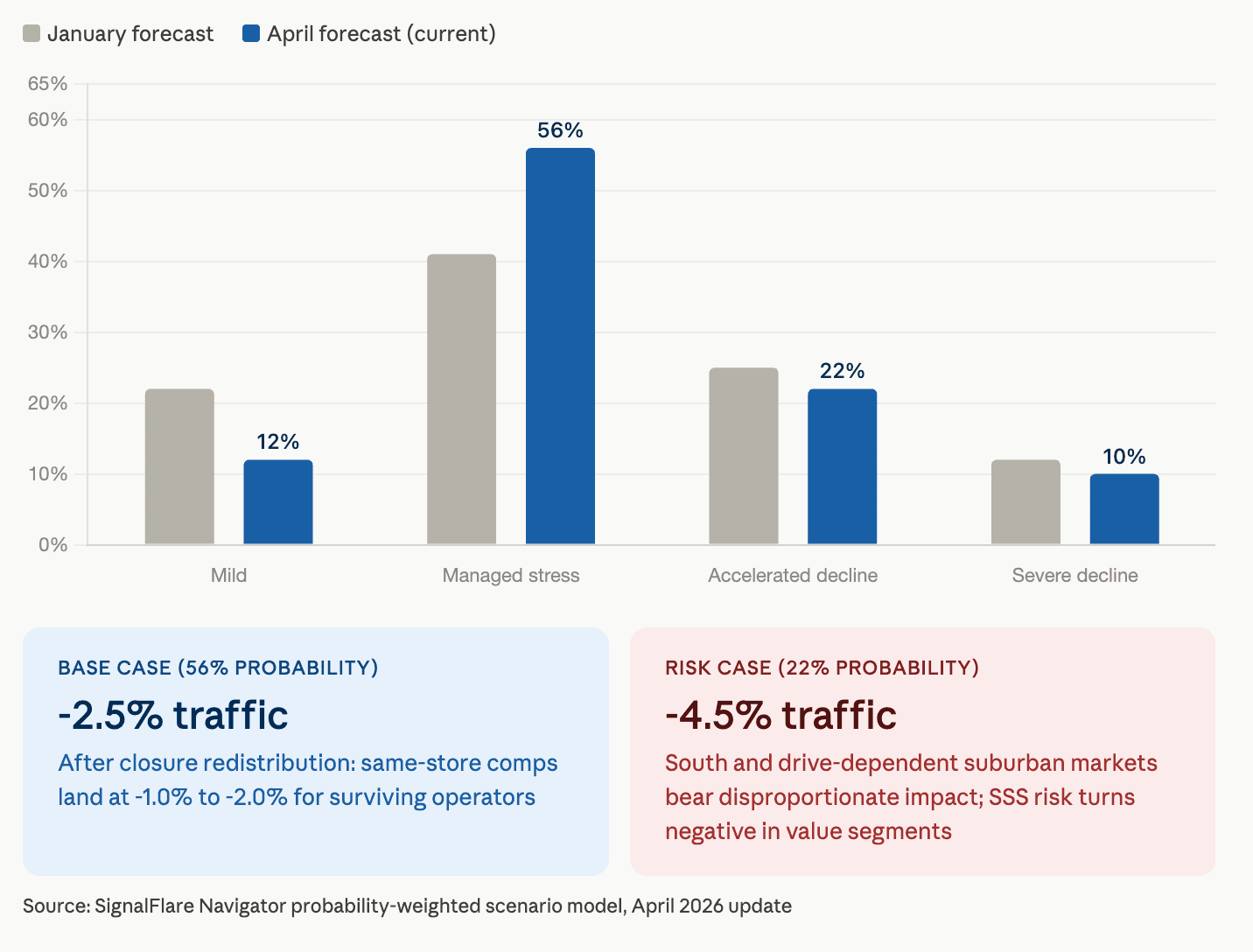

In January, the structural case alone generated a probability-weighted forecast of negative 3.2 percent and a 92 percent probability of negative traffic for the full year. The March CPI data and March industry traffic reading of negative 2.0 percent are now in the model. The updated probability-weighted forecast for late Q2 lands at negative 2.5 percent.

The scenario distribution has shifted. Managed Stress — defined as an environment where operators absorb the headwind through value positioning and menu rationalization without broad closure acceleration — is now the modal scenario at 56 percent probability, up from 41 percent in January. For surviving operators, the picture is better still. Closure redistribution adds an estimated 0.5 to 1.5 percentage points to same-store comps, putting the practical range at negative 1.0 to negative 2.0 percent under the base case.

Whether March’s negative 2.0 percent traffic reading reflects a better-than-expected hold or an incomplete read — the six-to-eight week gas lag puts the full weight of the March price spike squarely on May and June — will be visible in Q2 actuals. April is a transition month, not a read.

The South is where the downside scenarios carry the most real-world weight — the largest regional gas exposure, the highest drive-dependence, and a pre-existing 7.7 percentage point demographic traffic gap relative to the national baseline. The Northeast enters from the opposite position: below-national gas exposure, highest transit utilization, most insulated of any region.

Three data inputs will update the model heading into Q2: Q1 industry traffic actuals, the March retail sales report releasing April 21, and the trajectory of Brent crude. One additional variable is entering the tracking framework — restaurant closures within individual trade areas are showing a consistent directional signal at the store level, redistributing captive traffic to surviving competitors in ways that create real same-store comp opportunity for operators paying attention. The pattern is not yet statistically robust at scale, but it is consistent enough to weight more heavily as market rationalization accelerates.

Forward Planning

The industry was already operating under structural pressure before March. The energy shock has added a measurable incremental headwind — roughly 1.9 percent nationally and 2.5 percent in the South — with the full weight landing in May and June.

Revise pro-formas now. Any traffic or margin assumptions built before the March CPI release are stale. Re-run them with fuel surcharge pass-throughs and a consumer spending model that accounts for the gas price drag.

Watch the South and suburban trade areas first. Drive-dependent locations with lower-income consumer concentration will show the impact earliest and hardest.

Price with data, not instinct. The temptation to pass through input cost increases is understandable. The consumer’s willingness to absorb them is lower than it was 60 days ago. Test, measure, adjust.

Track the lag, not the headline. The April and May CPI reports will tell you where supply chain costs are headed. The March report told you where consumer sentiment is going. Both matter. Neither is sufficient alone.

Data sources: Bureau of Labor Statistics Consumer Price Index, March 2026 release; BLS Regional CPI Supplemental Tables; Bureau of Economic Analysis Consumer Expenditure Data; Energy Information Administration Crude Oil and Gasoline Spot Price Data; University of Michigan Surveys of Consumers, April 2026; U.S. Census Bureau Population Estimates Program; SignalFlare Navigator transaction, consumer behavior, and scenario probability model.

Share